Blockchain technology is revolutionizing the way transactions are conducted online. In this guide, we will walk you through the basics of blockchain technology and how you can use it to secure your data, financial transactions, and more. If you’re new to blockchain and want to know more about what it is and how it works, check out this What is Blockchain? Definition, Examples and How it Works article first.

Exploring Types of Blockchain Technology

Any

- blockchain enthusiast knows that there are various types of blockchain technology available in the market today. Each type has its unique features and functionalities that cater to different needs and requirements. In this chapter, we will research into the different types of blockchain technology to help you understand their differences and applications.

Though.

Public Blockchains

You might have heard of public blockchains such as Bitcoin and Ethereum. These blockchains are decentralized, open networks where anyone can participate, transact, and view the transaction history. Public blockchains are transparent, secure, and resistant to censorship. They are ideal for applications that require a high level of transparency and immutability.

Private Blockchains

An increasing number of organizations are exploring the potential of private blockchains for their operations. In a private blockchain, access is restricted to selected entities, making it suitable for businesses that require more control over who can join the network and access data. Private blockchains offer greater privacy, scalability, and efficiency compared to public blockchains.

The

Consortium Blockchains

The consortium blockchains strike a balance between public and private blockchains. In a consortium blockchain, a group of organizations come together to validate transactions and maintain the network. These blockchains are semi-decentralized, offering the benefits of both public and private blockchains. Consortium blockchains are suitable for industries where multiple stakeholders need to collaborate while maintaining a certain degree of control.

Plus,

Hybrid Blockchains

On the other hand, hybrid blockchains combine the features of public and private blockchains. They allow for a customizable level of control over who can participate in the network and access data. Hybrid blockchains are versatile and can be tailored to suit a wide range of use cases, offering the benefits of both public and private blockchains.

Hybrid blockchains are emerging as a popular choice for businesses looking to leverage blockchain technology while maintaining flexibility and control over their operations. With hybrid blockchains, organizations can enjoy the security and transparency of public blockchains, combined with the privacy and efficiency of private blockchains. This hybrid approach offers the best of both worlds, making it a compelling option for various industries and applications.

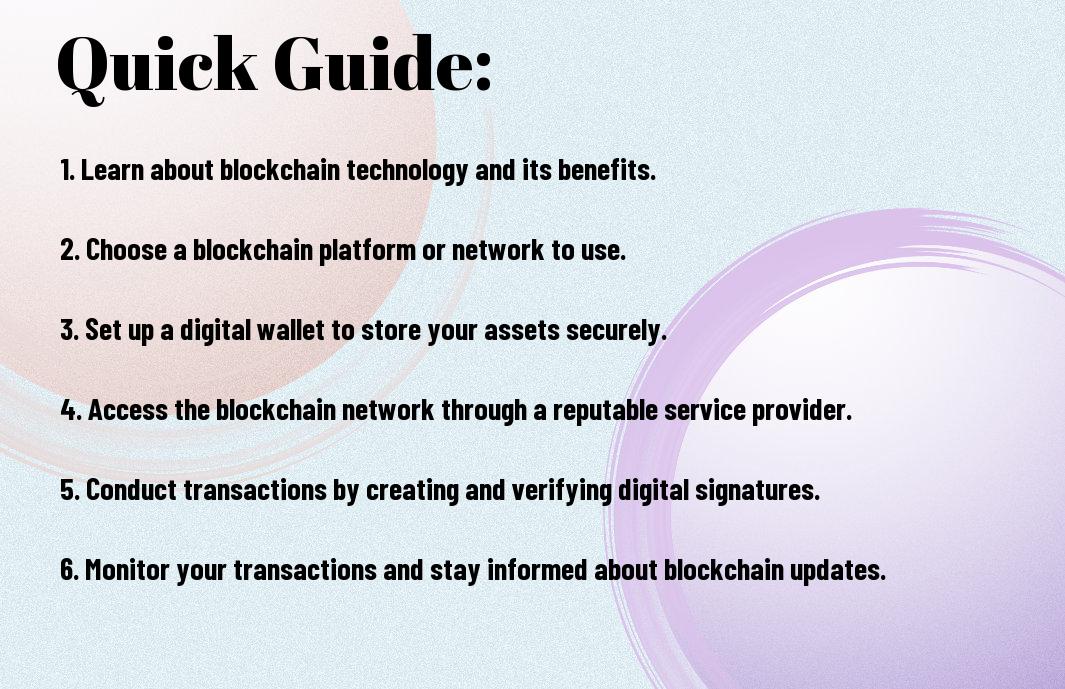

Step-by-Step Guide to Using Blockchain

| Identifying the Objective | Choosing the Right Type of Blockchain |

Identifying the Objective

On your journey to using blockchain technology, the first step is to identify the objective you want to achieve. Determine what problem you are trying to solve or what process you want to streamline with blockchain.

Choosing the Right Type of Blockchain

Objective clarity is key when it comes to choosing the right type of blockchain. Consider factors such as whether you need a public or private blockchain, the level of decentralization required, and the consensus mechanism that aligns with your goals.

This step lays the foundation for the entire blockchain implementation process. It is crucial to select the most suitable type of blockchain that aligns with your specific needs and objectives.

Setting Up the Blockchain Infrastructure

Setting up the blockchain infrastructure involves configuring the network, nodes, and establishing the necessary protocols. This step is vital to ensure the smooth operation of the blockchain network.

Choosing the right infrastructure provider and setting up secure connections are vital components of this process. This will help in ensuring the security and reliability of your blockchain network.

Implementing Smart Contracts

Even though it may sound complex, implementing smart contracts is crucial for automating processes and enhancing transparency in blockchain applications. Smart contracts are self-executing contracts with the terms of the agreement directly written into code.

Using smart contracts can streamline operations, reduce the need for intermediaries, and improve overall efficiency. Make sure to thoroughly test your smart contracts before deploying them to the blockchain network.

Handy Tips and Factors to Consider

All stakeholders interested in utilizing blockchain technology should take note of the following handy tips and factors before venturing into implementation. After considering these aspects, your blockchain journey will be more successful and efficient.

Tips for Smooth Blockchain Integration

With proper planning and execution, integrating blockchain technology into your business processes can be a seamless experience. Remember to involve key stakeholders, conduct thorough training sessions, and continuously monitor performance metrics. This will ensure a smooth transition and adoption process.

Critical Factors in Blockchain Deployment

Little oversight on critical factors can lead to complications in blockchain deployment. Key aspects to consider include scalability, security measures, and regulatory compliance. Perceiving these factors will help in ensuring the success of your blockchain implementation.

- Scalability

- Security

- Regulatory Compliance

Blockchain technology holds tremendous potential for revolutionizing various industries, but it also comes with risks and challenges. It is crucial to prioritize scalability to accommodate increased transaction volume, implement robust security measures to safeguard sensitive data, and ensure compliance with regulatory standards. Perceiving these critical factors and addressing them proactively will enhance the effectiveness and longevity of your blockchain deployment.

Weighing The Pros and Cons

| Pros | Cons |

|---|---|

| Increased Security | High Energy Consumption |

| Transparency | Scalability Challenges |

| Decentralization | Regulatory Uncertainty |

| Immutability | Integration Complexity |

| Efficiency | Potential for Illegal Activities |

Advantages of Embracing Blockchain

You can benefit from increased security, transparency, decentralization, immutability, and efficiency by embracing blockchain technology. These features provide a reliable and tamper-proof system for transactions and data management.

Potential Drawbacks to Consider

With the adoption of blockchain technology, it is crucial to consider the high energy consumption, scalability challenges, regulatory uncertainty, integration complexity, and the potential for illegal activities that may arise. Understanding these drawbacks can help in making informed decisions when implementing blockchain solutions.

Advantages: It is important to note that despite the drawbacks, the benefits of enhanced security, transparency, and efficiency often outweigh the challenges associated with blockchain technology. By carefully weighing the pros and cons, businesses can leverage blockchain effectively to improve their operations.

To wrap up

Now that you have a better understanding of how to use blockchain technology, you can start exploring its endless possibilities. Whether you are interested in secure transactions, transparent supply chains, or decentralized applications, blockchain has something to offer for everyone. Keep learning and experimenting with this innovative technology to discover how it can benefit your business or personal projects. Embrace the future of decentralized, secure, and transparent systems with blockchain technology!

FAQ

Q: What is Blockchain Technology?

A: Blockchain technology is a decentralized, distributed ledger that securely records transactions across a network of computers. It enables transparent, tamper-proof, and verifiable transactions without the need for intermediaries.

Q: How does Blockchain Technology work?

A: Blockchain technology works by creating a chain of blocks that contain transaction data. Each block is linked to the previous one, forming a secure and immutable record. Transactions are validated by network participants through consensus mechanisms like Proof of Work or Proof of Stake.

Q: What are some common applications of Blockchain Technology?

A: Blockchain technology is used in various industries, including finance for secure payments and smart contracts, supply chain management for transparent tracking of goods, healthcare for secure sharing of patient data, and voting systems for transparent and tamper-proof elections.